Welcome to Safe as Houses, a series delving into a topic close to the heart of many Australians – property. This is not a series on where the market might be heading. Instead we aim to explore how we view property and float some alternative ideas.

Along with poorly behaved sporting figures, Kyle Sandilands, and casual police brutality, crushingly large mortgages are basically accepted as an unpleasant fact of life.

But what if we could change the way we repaid our loans to pay less interest and enjoy improved home affordability? Adjunct Associate Professor at the University of Canberra, Kevin Cox explains how.

In The Conversation this week, Keith Jacobs argues that falling house prices would lead to positive outcomes for the Australian economy. Here I propose a way to reduce the cost of housing that will, over time, also reduce house prices.

A reason for unaffordable housing is that the finance costs of purchasing a house with a loan is at least twice as much as it needs to be. Reducing the cost of finance will reduce the total cost of purchasing a house. This will, in turn, reduce the pressure on house prices as it will reduce the financial profitability of traditional housing loans and direct finance to other more productive and profitable uses.

Most loans are used to transfer control of an asset from one person to another. The person receiving the loan agrees to pay rent for the use of the asset while ever they have the use of the asset. When they relinquish control of the asset they no longer pay rent on the asset. Let us assume the asset is a fleet of five cars. A borrower rents five motor cars and so pays rent on five cars. If they return one car they pay rent on the four remaining cars and they do not pay rent on the returned car.

Money loans work differently. Let us assume that the rent on five units of money is one unit of money. If one unit of money is returned then rent is continued to be paid on five units of money - not four. We treat money loans differently from other asset loans because we create money with an interest coupon attached at the time of creation. This gives money a value over time by the way it was created. Money when it is saved should have an interest coupon attached. Money when it is created should not have an interest coupon attached.

Most people think banks take in deposits and lend the deposits. Unfortunately this is not the way the system works. When a bank gives a loan the bank creates new money to lend. This money is deposited in the borrower’s account. There was no deposit lent or money saved - instead the bank created money and deposited it. This newly created money immediately attracts interest. This is the underlying reason why, in the above example, rent continues to be paid on five units not four because banks have to pay interest on newly created money.

Because we create money with an interest coupon and because interest itself attracts interest then the amount of money needed to keep the system operating compounds. In the ancient world the Sumerians, Babylonians, Jews and Romans understood the unsustainable nature of debt and periodically they had a debt jubilee to remove the excess debt. Muslims and Christians tried to solve the problem by banning interest.

There is another solution. We can change the rules on how to repay loans. We continue to pay rent (interest) on money but pay no interest on accumulated interest.

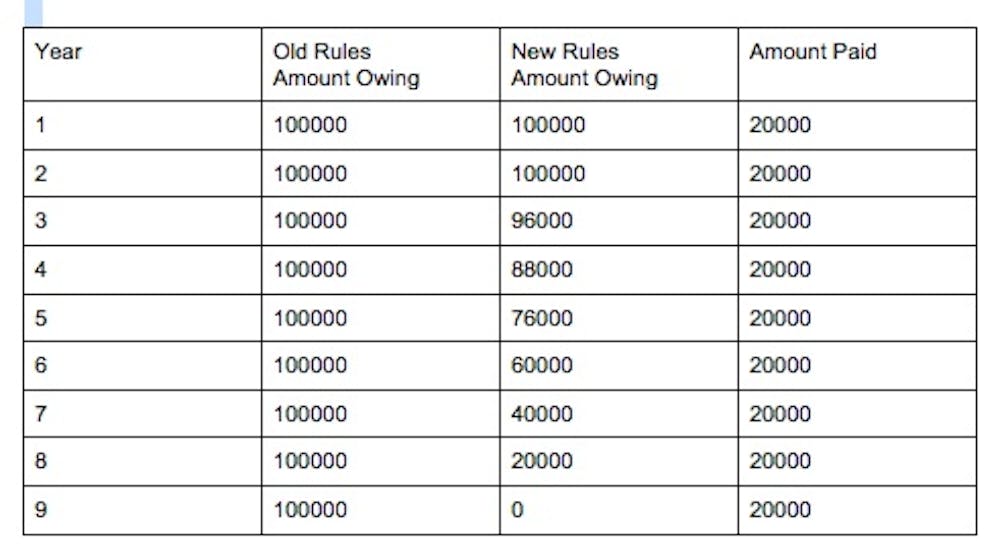

Using existing loan repayment rules, if we have a loan of $100,000 with a yearly interest rate of 20% and we repay $20,000 each year then the loan is never repaid. Each year the $20,000 repayment does not reduce the capital on which interest is paid and it means we pay interest on the money that has been repaid. The new proposed rules of repayment are for repayments to come off the principal and no interest is to be charged on unpaid interest.

At the end of the first year, with these new rules, the borrower still owes $100,000 but the amount of money on which interest is paid in the next year is $80,000. This means that at the end of the second year the amount owed is $96,000. Each year the amount owed will reduce until finally the debt is repaid. With both sets of rules the same amount has been paid so the economic outcomes are the same. The difference is that the new rules extinguish the debt.

This simple change to repayment rules could make a dramatic change in the cost of capital goods financed through loans. For example, the interest charges on a home loan of $500K at 7% over 30 years is about $611,000 while the total interest charges on a loan with revised rules with the same size repayments is $225,000.

If the approach is adopted it will mean that housing in Australia will become affordable without a collapse in house prices.

In systems terms the positive feedback mechanism of interest on interest has been removed. In most systems positive feedback almost always leads to instability. Removing mechanisms that cause positive feedback means the system has a better chance of stabilising. What this means for house prices is that the inflationary pressures will be reduced.

For banks, it means they will find it more profitable to lend existing deposits for housing rather than create new deposits with new money. However, money still needs to be created so banks will have deposits to lend. (I describe one way to do this in a previous article. )

In summary, the issuing of credit through the creation of interest bearing money leads to a compounding of debt, which unnecessarily increases the cost of credit.

By changing loan repayment rules, the cost of credit is reduced which reduces the cost to transfer capital assets to the benefit of both the buyer and seller.

This is the fourth article in the Safe as Houses series. Read the other instalments here: